On March 6, 2024, the U.S. Securities and Exchange Commission (“SEC”) adopted a long-awaited final rule, The Enhancement and Standardization of Climate-Related Disclosures for Investors, which will require registrants, including foreign private issuers (“FPIs”),[1] to disclose extensive climate-related information in their registration statements and periodic reports (the “Final Rule”). The Final Rule is intended to facilitate the disclosure of “complete and decision-useful information about the impacts of climate-related risks on registrants” and to improve “the consistency, comparability, and reliability of climate-related information for investors.” The Final Rule constitutes one of the most significant changes ever to SEC disclosure requirements, and is expected to face legal challenges. The Final Rule is available here and the accompanying fact sheet is available here.

The SEC delayed the finalization of the proposed rule (the “Proposed Rule”) past the original expected date of October 2022, after receiving over 22,500 comment letters.

As the Final Rule is extensive, this Client Update focuses on summarizing key aspects of the Final Rule. In a subsequent update, we will analyze key changes from the Proposed Rule and provide practical tips for registrants to prepare to comply with the Final Rule.

COMPLIANCE DATES

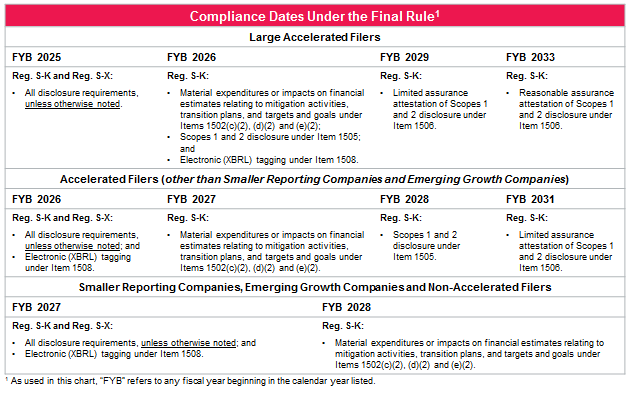

The Final Rule includes phase-in dates for compliance. The initial compliance phase-in is based on filer status, with additional phase-ins for disclosure of material expenditures and GHG reporting, as well as for the attestation requirement and the level of assurance required in the attestation report. The Final Rule does not provide an exemption or transitional relief for registrants conducting an initial public offering.

A chart outlining the compliance dates can be found here.

Key Requirements

- Scope 1 and Scope 2 GHG Emissions. Large accelerated filers (“LAFs”) and accelerated filers (“AFs”) that are not smaller reporting companies (“SRCs”) or emerging growth companies (“EGCs”) are required to disclose, if material, their Scope 1 greenhouse gas (“GHG”) emissions (direct emissions from operations that are owned or controlled by the registrant) and Scope 2 GHG emissions (indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the registrant) on a phased-in basis. This is a departure from the Proposed Rule, which would have required such disclosures regardless of materiality. Such disclosure must cover emissions for the registrant’s most recently completed fiscal year and, to the extent previously disclosed, for the historical fiscal year(s) included in the filing. In a related change from the Proposed Rule, GHG emissions disclosure will not be required for private companies that are parties to business combination transactions involving Forms S-4 and F-4.

In response to commenter concerns regarding the timing for compliance with GHG emissions disclosure requirements, the Final Rule provides that any GHG emissions disclosure required to be included in an annual report on Form 10-K may be incorporated by reference from the registrant’s quarterly report on Form 10-Q for the second fiscal quarter of the fiscal year in which such annual report is due. For FPIs, any GHG emissions disclosure required to be disclosed in an annual report on Form 20-F may be disclosed in an amendment to Form 20-F, which will be due no later than 225 days after the end of the previous fiscal year.

Any GHG emissions disclosure required to be included in a registration statement pursuant to the Securities Act of 1933, as amended, or Exchange Act must be provided as of the most recently completed fiscal year that is at least 225 days prior to the date of effectiveness of the registration statement.

Following a phase-in period, LAFs and AFs (other than SRCs and EGCs), including FPIs, must obtain and include with their filings an attestation report from an independent attestation service provider covering the registrant’s Scope 1 and Scope 2 GHG emissions. The minimum level of assurance required will be “limited assurance” beginning the third fiscal year after the GHG emissions disclosure compliance dates. Additionally, LAFs will be required to obtain an attestation report at the “reasonable assurance” level beginning the seventh fiscal year after the GHG emissions disclosure compliance date.

- Scope 3 GHG Emissions. In a significant departure from the Proposed Rule and in response to “concerns about the current availability and reliability of the underlying data for Scope 3 emissions,” registrants are not required to disclose Scope 3 GHG emissions (all other indirect GHG emissions that occur in the upstream or downstream activities in the registrant’s value chain).

- Financial Statement Disclosure (Regulation S-X Amendments). Registrants must disclose information on the impact of climate-related risks on their business and in a footnote to their consolidated financial statements. This includes:

– a qualitative description of how the development of estimates and assumptions used in producing financial statements were materially impacted by risks and uncertainties associated with severe weather events and other natural conditions; and

– disclosure, for the fiscal years presented, of the separate aggregate amounts of (i) expenditures expensed, (ii) capitalized costs and (iii) losses related to each of (a) severe weather events and other natural conditions, subject to applicable one percent and de minimis disclosure thresholds and (b) carbon offsets and renewable energy credits or certificates if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals.

- Impacts of Climate-Related Risks (Qualitative Disclosure). Registrants are required to describe any climate-related risks identified by the registrant that have had, or are reasonably likely to have, a material impact on the registrant, including on its strategy, results of operations or financial condition in the short term (e., the next 12 months) and in the long term (i.e., beyond the next 12 months), as well as the actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model and outlook, including, as applicable, any material impacts on a non-exclusive list of items included in the Final Rule.

- Risk-Management Disclosure. If a material climate-related risk is identified, registrants are required to describe their processes for identifying, assessing and managing such material climate-related risks, as well as whether and how those processes are integrated into the registrant’s overall risk management program. Registrants must also disclose how they will manage identified climate-related risks, including (i) identifying whether a material physical or transition risk has been or is reasonably likely to be incurred, (ii) deciding whether to mitigate, accept or adapt to a particular risk and (iii) deciding how to prioritize the climate-related risk.

- Corporate Governance Disclosure. Registrants must describe the oversight and governance of climate-related risks by the board and management in their Forms 10-K and 20-F, as applicable. In response to commenter concerns, the Final Rule streamlines the enumerated disclosure elements that were initially proposed and dispenses with some prescriptive elements of the Proposed Rule (including that registrants identify specific board members responsible for climate-related oversight or describe the expertise in climate related risks of any board members, each if applicable). With respect to the board, registrants must identify, to the extent applicable, (i) any board committee or subcommittee responsible for the oversight of climate-related risks; (ii) a description of the process by which the board or such committee or subcommittee is informed about such risks; and (iii) whether and how the board oversees progress against targets, goals or transition plans disclosed pursuant to the Final Rule. These disclosures are not required for registrants whose boards do not exercise board oversight of climate-related risks.

With respect to management, registrants must describe management’s role in assessing and managing material climate-related risks, including by addressing, to the extent applicable, (i) whether and which management positions or committees are responsible for assessing and managing such risks; (ii) management processes for assessing and managing such risks; and (iii) board reporting processes. Consistent with the SEC’s approach to analogous disclosure requirements relating to cybersecurity, registrants must disclose the relevant expertise of members of management responsible for assessing and managing climate-related risks. Consistent with the board disclosures described above, these disclosures are not required for registrants that do not engage in the oversight of material climate-related risks.

- Registrant Climate Policy-Specific Disclosures. Registrants must disclose climate-related targets and goals, scenario analyses, internal carbon pricing and transition plans, to the extent that these tools are used by the registrant. In a departure from the Proposal Rule, in each case, the Final Rule conditions the disclosure on materiality.

If registrants have set climate-related targets or goals that have materially affected or are reasonably likely to materially affect a registrant’s business, results of operations or financial condition, registrants must make certain disclosures about such targets or goals, including material expenditures and material impacts on financial estimates and assumptions as a direct result of such targets or goals or actions taken to make progress toward meeting such targets or goals. The Final Rule provides a non-exhaustive list of examples of such additional information, which includes: (i) the scope of activities included in the target or goal; (ii) the unit of measurement; (iii) the defined time horizon by which the target or goal is intended to be achieved; (iv) the defined baseline time period and the means by which progress will be tracked; and (v) how the registrant intends to meet climate-related targets or goals.

The Final Rule provides that, if a registrant uses scenario analysis to assess the impact of climate-related risks on its business, results of operations, or financial condition, and if, based on the results of scenario analysis, a registrant determines that a climate-related risk is reasonably likely to have a material impact on its business, results of operations, or financial condition, then the registrant must describe each such scenario, including a brief description of the parameters, assumptions, and analytical choices used, as well as the expected material impacts, including financial impacts, on the registrant under each such scenario.

If applicable, registrants are required to disclose certain information about their use of carbon offsets or renewable energy certificates, to the extent they are used as a material component of a registrant’s plan to achieve climate-related targets or goals.

If registrants have adopted a transition plan to manage a material transition risk, they must (i) provide a description of the transition plan, (ii) update disclosures in the subsequent years describing the actions taken during the year under the plan, including how the actions have impacted the registrant’s business, results of operations or financial condition, and (iii) disclose quantitative and qualitative disclosure of material expenditures incurred and material impacts on financial estimates and assumptions as a direct result of the disclosed actions. Unlike the Proposed Rule, the Final Rule does not enumerate transition risks and factors related to those risks that must be disclosed. Registrants must update transition risk disclosures annually in their Forms 10-K or 20-F, as applicable.

- Private Securities Litigation Reform Act (“PSLRA”) Safe Harbor. The Final Rule extends the PSLRA’s statutory safe harbor for forward-looking statements to disclosure (excluding historical facts) pertaining to transition plans, scenario analysis, the use of internal carbon pricing, and targets and goals. Statements made by issuers and/or in connection with certain transactions that are currently excluded from the PSLRA safe harbor for forward-looking statements (such as registrants conducting an initial public offering) will nevertheless be eligible for the safe harbor provided by the Final Rule.

We expect there to be legal challenges to the Final Rule on both administrative and constitutional grounds, which may affect the compliance dates for the Final Rule. In fact, on the same day the SEC voted to approve the Final Rule, a coalition of ten states led by West Virginia filed a petition for review of the Final Rule in the United States Court of Appeals for the Eleventh Circuit. The petition states that the petitioners “will show that the final rule exceeds the agency’s statutory authority and otherwise is arbitrary, capricious, an abuse of discretion, and not in accordance with law.”[2]

***

This was originally published here.

***

To subscribe to our ESG Weekly Update, please click here.

***

To subscribe to the Debevoise Fintech Blog, click here.

***

[1] The Final Rule does not apply to Canadian registrants that use the Multijurisdictional Disclosure System and file their registration statements and annual reports on Form 40-F under the Securities Exchange Act of 1934, as amended.

[2] Petition for Review, State of W. Va., et. al. v. SEC, No. 24-_____ (11th Cir.).

{kind=link}